Week 5 — Bootstrap distributions

Resampling with replacement, and how a statistic wobbles

Source basis. Original instructor-authored notes; data is synthetic (30 “repair times” drawn from a fixed generator, seed 45205). Open texts are conceptual companions cited by section title only (map-don’t-mine); no prose, figures, examples, or exercises are reproduced. See Open readings & attribution. Ungraded — Blackboard is authoritative for graded work.

This week. Last week we produced a p-value by simulating what the data could have looked like under a null. This week we ask a different question about a single sample: how much would our summary have wobbled if we had drawn a different sample? The bootstrap answers it by treating the sample as a stand-in for the population and resampling from the sample itself.

Learning goals

By the end of this week you should be able to:

- Explain what resampling with replacement does, and why a bootstrap distribution approximates sampling variability.

- Build a bootstrap distribution of a statistic (here, the median) and read its spread and a percentile interval.

- Keep three things distinct: the data, the bootstrap distribution, and the (usually unseen) true sampling distribution.

- State what the bootstrap assumes — and name a statistic for which it fails.

Where we are

We keep returning to one question: what is fragile here, and what can we still say? A single number like a sample median is fragile in a specific way — draw a different sample and you would get a different median. Ordinarily we never see that variability, because we only have one sample.

The bootstrap’s move is almost cheeky: if the sample is our best picture of the population, then drawing new samples from the sample (with replacement, same size) imitates drawing new samples from the population. Each resample gives a new value of the statistic; the collection of those values is the bootstrap distribution, and its spread estimates how much the statistic wobbles.

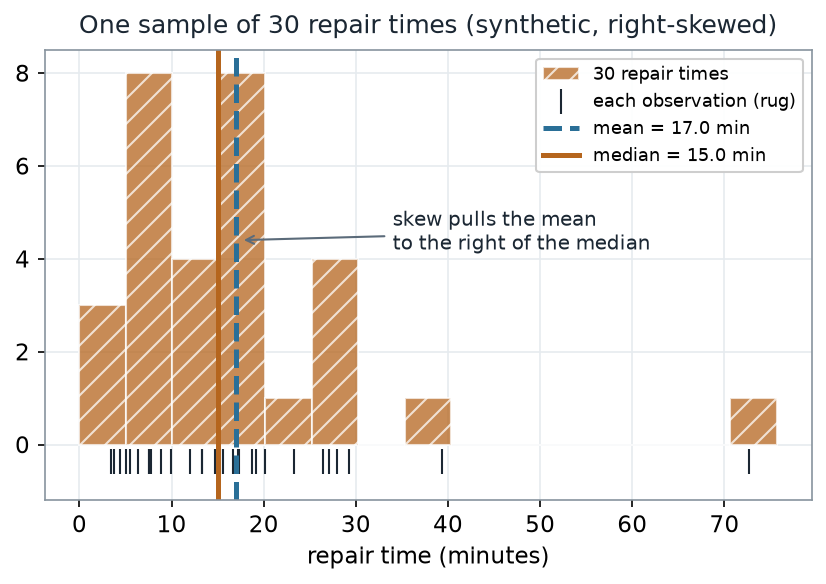

The sample we will resample

Our running example is a batch of 30 repair times (minutes), synthetic and right-skewed. Because the data is skewed, the mean is pulled to the right of the median — so the median is the steadier summary, and it is the one we will bootstrap.

What to notice. The sample is right-skewed, so the mean (17.0 min) sits above the median (15.0 min). A handful of long repairs drag the mean up; the median barely moves. That resistance is exactly why we summarize this sample with the median.

The sample, as numbers (nonvisual equivalent).

| Summary | Value (minutes) |

|---|---|

| n | 30 |

| Min · Q1 · Median · Q3 · Max | 3.4 · 7.6 · 15.0 · 19.9 · 72.7 |

| Mean | 17.0 |

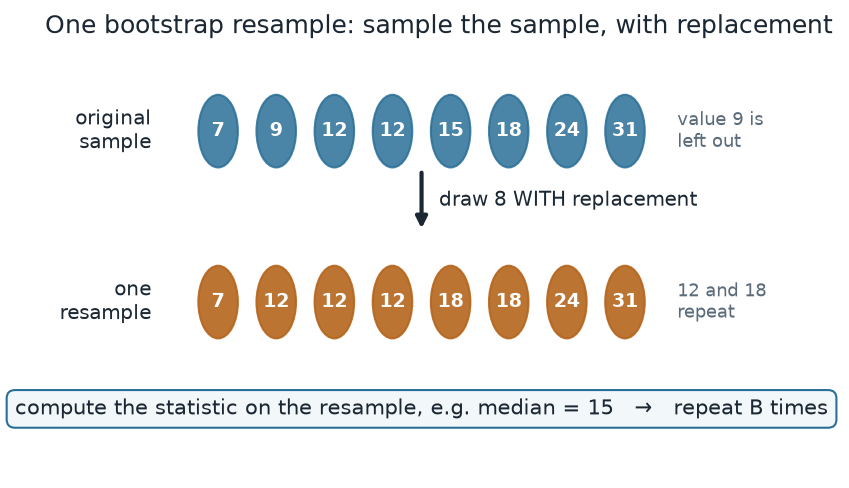

How one bootstrap resample works

A single bootstrap resample is one mechanical move: draw a sample of the same size from the observed values, with replacement. Some values get picked more than once; others get left out.

What to notice. The bootstrap samples from the sample, not from the population. Value 9 dropped out of this resample; 12 and 18 repeat (12 three times, 18 twice). Repeat this thousands of times, recomputing the statistic each time, and the spread of those recomputed values is the bootstrap distribution.

The demo, as numbers. Original sample 7, 9, 12, 12, 15, 18, 24, 31 → one resample 7, 12, 12, 12, 18, 18, 24, 31 → resample median 15.

The R you would run is short — and notice there is no plotting in it; the picture is downstream:

# Schematic: the named data objects are the sample(s) described in the text above; this illustrates the analysis, not a self-contained runnable block.

# resample the sample, with replacement, and recompute the statistic

set.seed(45205)

x <- repair_times # the 30 observed values

B <- 2000

med <- replicate(B, median(sample(x, size = length(x), replace = TRUE)))

sd(med) # bootstrap standard error of the median

quantile(med, c(0.025, 0.975)) # a 95% percentile interval (Week 6 builds on this)Worked example — bootstrapping the median

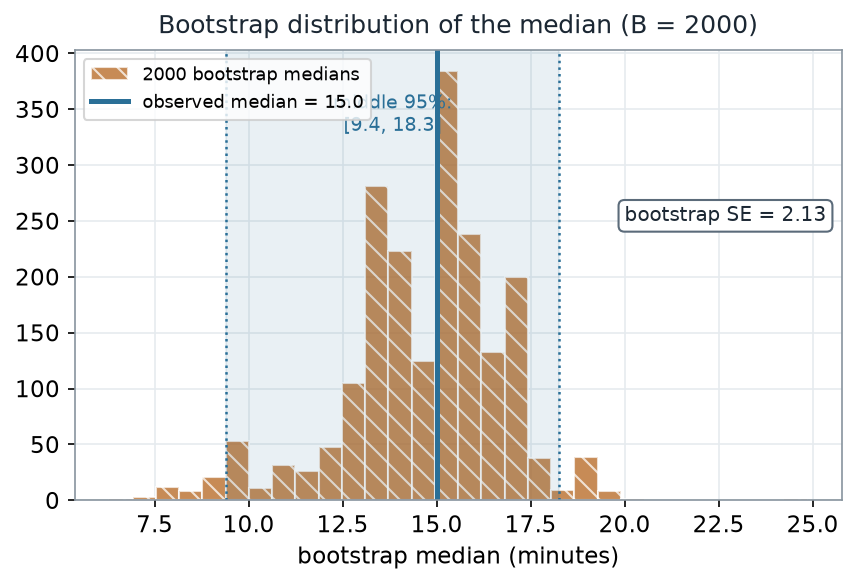

Running the resampling above 2000 times gives a bootstrap distribution of the median.

What to notice. The width of this distribution is the point. The observed median (15.0) is not exact — resampling shows it would plausibly have landed anywhere across roughly 9 to 18 minutes. The standard deviation of the bootstrap medians, about 2.1 minutes, is the bootstrap standard error of the median.

Bootstrap read-out (nonvisual equivalent).

| Quantity | Value |

|---|---|

| Observed median | 15.0 min |

| Bootstrap SE of the median | 2.13 min |

| Middle 95% (percentile) | [9.4, 18.3] min |

| Resamples (B) | 2000 |

What the bootstrap is really doing

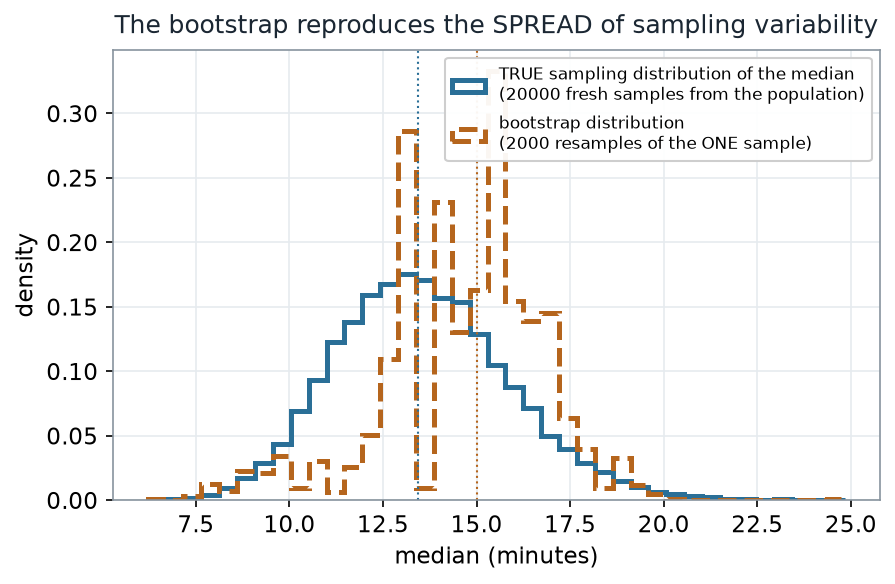

Here is the honest question: does that bootstrap distribution actually match the true sampling variability of the median? Because our data is synthetic, we know the population, so for once we can draw the true sampling distribution (take 20,000 fresh samples of 30 from the population and take each median) and lay it beside the bootstrap.

What to notice. Similar width, different center. The bootstrap reproduces the spread of sampling variability remarkably well from a single sample — bootstrap SE 2.13 vs the true sampling SE 2.31. But it is centered where the sample happened to land (15.0), not at the truth (13.4). The bootstrap estimates variability, not the parameter. If your one sample is off-center, so is your bootstrap.

Spread vs center (nonvisual equivalent).

| Distribution | Center | SE (spread) |

|---|---|---|

| True sampling distribution of the median | ≈ 13.4 (true) | 2.31 |

| Bootstrap distribution (from the one sample) | 15.0 (observed) | 2.13 |

A common mistake

“Nonparametric and resampling-based, so the bootstrap has no assumptions.” It has real ones. It assumes your sample is a fair stand-in for the population and that observations are independent — and it leans on the sample being large enough to carry the shape you need. When those slip, so does the bootstrap. The clearest failure is an extreme order statistic like the maximum.

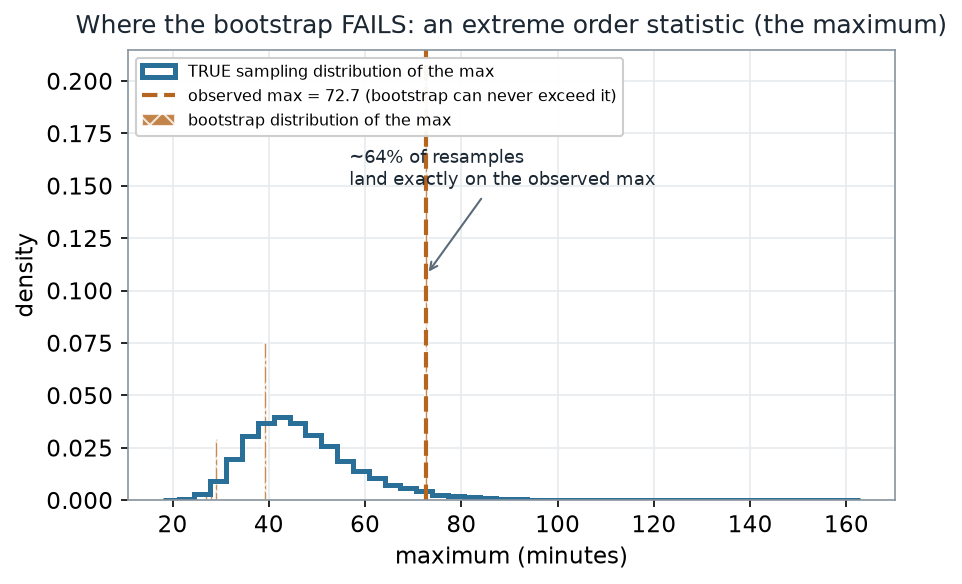

Worked example — where the bootstrap fails

Bootstrap the maximum of the same 30 values instead of the median, and compare again to the truth.

What to notice. A resample can only reuse values you already have, so its maximum can never exceed the observed maximum (72.7) — and about 63% of resamples hit that value exactly (that is \(1 - (1 - 1/n)^n \approx 0.63\) for \(n = 30\)). The result is a lumpy, capped distribution that misses the smooth truth entirely. The bootstrap is a tool with a domain, not a universal solvent.

Failure read-out (nonvisual equivalent).

| Quantity | Value |

|---|---|

| Observed maximum | 72.7 min |

| Share of resamples whose max equals the observed max | 0.63 |

| Can a bootstrap max exceed 72.7? | No |

Check your understanding (ungraded)

- In your own words, what is the bootstrap sampling from, and why must a resample be the same size as the original sample?

- The bootstrap SE of the median came out near 2.1 minutes. What real-world quantity is that number an estimate of?

- The bootstrap distribution of the median matched the true one’s spread but not its center. Explain why, and what that means for how much you should trust the observed median as the “answer.”

- Give one reason the bootstrap of the maximum failed, and name one other statistic you would be cautious bootstrapping.

Reading guide

- IMS — Bootstrapping — a conceptual companion to the resample-with-replacement idea; read for the intuition, then verify it against the picture above.

- OpenIntro Statistics 4e — foundations for inference — reinforces sampling variability as the thing the bootstrap approximates.

- Hesterberg (2015), What Teachers Should Know About the Bootstrap — an instructor reference on what the bootstrap does and does not deliver (cited, not reproduced).

Accessibility notes

Mathematics is live text (\(1 - (1-1/n)^n\) renders as MathML, not an image). Every figure carries an alt line stating its message, a “what to notice” reading, and an adjacent data-summary table, so each point survives without the picture. Distributions are distinguished by linestyle and hatch (solid = true, dashed/hatched = bootstrap) and labels, not color alone. A clean lint and a clean render are evidence; the rendered assistive-technology review is a human step.

Assessment (descriptive only)

This week contributes learning evidence toward building and reading a bootstrap distribution and naming what the bootstrap assumes. That is the shape only; the actual graded prompts, points, and due dates live in Blackboard.

Public vs. graded. These are public, ungraded notes and practice. Graded prompts, keys, rubrics, point values, and due dates live in Blackboard Ultra, which governs.

Looking ahead

Next week we turn this bootstrap distribution into a confidence interval — the percentile interval you already computed above — and ask the harder questions: what does the interval actually claim, and when does it fail?